Municipalities today are looking for alternative ways to fund essential services such as street improvements. Learn why transportation utility fees (TUFs) serve as a beneficial option and how raSmith is assisting communities in studying and successfully implementing TUFs.

What are TUFs?

Municipalities can leverage the advantages of transportation utility fees to fund roadway repairs.

The Federal Highway Administration defines TUFs as “a financing mechanism that treats the transportation system like a utility in which residents and businesses pay fees based on their use of the transportation system rather than taxes based on the value of property they occupy.” Also known as transportation user charges, street utility fees or road use fees, TUFs offer municipalities a viable method to pay for roadway maintenance and repairs. A TUF is typically included on monthly or quarterly utility bills sent to all property owners who have access to the community’s roadways.

How do TUFs work?

Since transportation system usage is not metered in the same manner as, for example, home electricity usage, TUFs are based on the number of trips generated by each property in the community. This number is most often calculated using trip-generation rates published by the Institute of Transportation Engineers (ITE) for various land uses. As such, the fees are applied to each property based on two factors:

- Access to each property as a benefit of the transportation system

- Traffic generated by each property as it contributes to the wear and tear, or degradation, of the transportation infrastructure in proportion to the number and types of vehicles that use it

Levy limits on property taxes and growing debt concerns challenge communities to sufficiently fund maintenance of their street infrastructure, particularly as many other municipal budget priorities compete for the same dollars. As a user-charge source, TUF revenues are dedicated solely to maintenance and reconstruction of the transportation infrastructure and cannot be used for other municipal purposes. Additionally, if TUFs are used to reduce borrowing for street reconstruction projects, the long-term cost savings to the community can be very substantial.

How does a TUF differ from a tax?

It is important to design and implement the TUF properly to meet these user charge criteria:

- Charges are for the services and facilities provided to customers, or users

- The basis for the charge must be reasonably related to the cost of the service or product

- Charges must be just and reasonable

- Charges may not be unjustly discriminatory

In contrast, property taxes are required and levied to raise general revenue for the broad operation and funding of government services. Property taxes are calculated in proportion to the assessed value of each individual property compared to the total assessed value of all taxed properties in a community, regardless of any related benefit or impact to the transportation infrastructure or any other service. Additionally, properties that are exempt from paying taxes benefit from the transportation system but do not contribute any revenue to help pay for its cost.

Since the purpose of a TUF is to help fund street maintenance and reconstruction at a level related to the cost of the service, individual user charges reflect the relative use and benefit of each property, including those that are exempt from property taxes. From a practical perspective, this means that the TUF charged to a convenience store is greater than that charged to a single-family home with the same assessed value because the store generates substantially more use of the transportation infrastructure. In contrast, the same two properties would pay equivalent property tax bills.

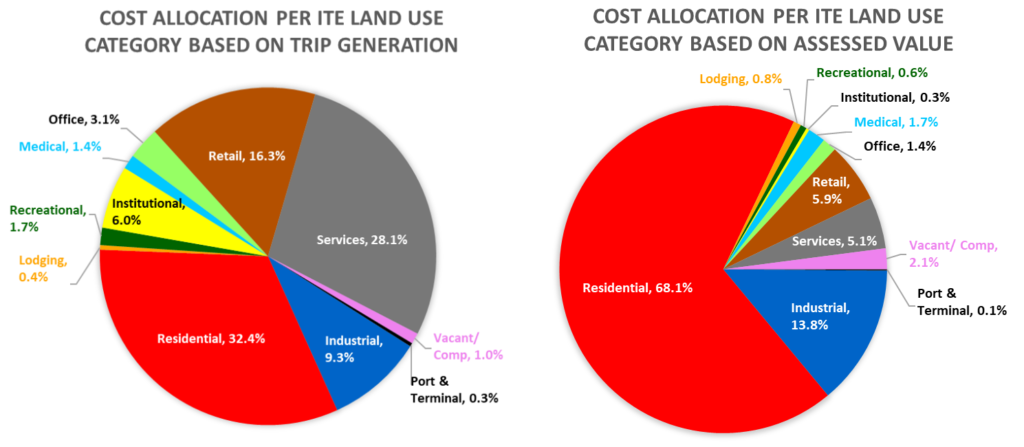

TUFs (trip generation) vs. property taxes (assessed value): a significant difference in cost allocations.

The above pie charts compare revenue generated by trip-generation-based TUFs to property tax revenues paid for all properties within the designated land use categories. The difference in cost allocations across various land use categories for the two methods is significant. Although individual land use category proportions vary among communities, the overall shift in allocations between the two funding mechanisms is significant.

In summary, there are many advantages of using TUFs to fund your transportation infrastructure:

- All properties in the community contribute

- Charges are equitable, proportionate to each property’s relative benefit and impact

- Revenues are dedicated to only the transportation infrastructure and its administration and provide a uniform revenue stream

- As a user charge, TUFs provide an alternative to long-term debt financing and related finance charges

This publication from the League of Wisconsin Municipalities provides additional details about funding street maintenance using TUFs, including state statute references.

We can help

raSmith’s team includes municipal engineers with municipal infrastructure design and maintenance experience, and traffic engineers who are very familiar with trip-generation rates and applications. Our team has developed extensive TUF models to determine annual charges to all properties in a community on a trip-generation basis, including compilation tools and statistics to support financial planning and analysis. raSmith staff is currently working with several Wisconsin communities at various stages of studying and implementing TUFs.

Learn more about raSmith’s municipal engineering services.